Passing on your wealth to the right people, at the right time.

Our advisers can help.

Expert Inheritance Advice & Planning Advisors in Oxfordshire & West Lothian

Leaving a legacy

There is a range of options that help reduce the potential tax liability on your death. Investing a little time and effort now means you can rest assured the people you want to leave your possessions and wealth to.

Our experts can help.

No Obligation Financial Health Check

Just a click away, we’ll be in touch

The internet is not a secure medium and the privacy of your data cannot be guaranteed.

An introduction to Inheritance Tax (IHT)

While most estates are too small to be subject to IHT, those valued above the current starting point of £325,000 face an average bill of £179,000.

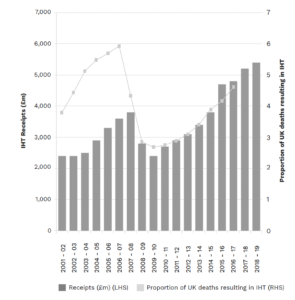

IHT is a complex system with its roots in the 1970s, when it was introduced as the successor to Estate Duty. However, rising house prices and a freeze on the IHT threshold have sharply increased the government’s tax take in recent years, as this chart shows.

The importance of estate planning

Successful estate planning helps you to better control the amount of tax you are liable to pay on the wealth you accumulate. You’ve worked hard to build up your current wealth. You may have taken risks, devoted long hours to building up your business, or made sacrifices to establish your investment portfolio.

At the same time, you’ve probably paid a significant amount of tax in the form of:

— Income tax — Corporation tax — Capital Gains Tax — Stamp Duty Land Tax — National Insurance — And then, of course, there’s Inheritance Tax (IHT).

HM Revenue and Customs practice and the law relating to taxation are complex and subject to individual circumstances and changes which cannot be foreseen.

While IHT may be a legitimate concern for you and your beneficiaries, there is more to estate planning than simply trying to reduce the Chancellor’s slice of your legacy. To start with, it’s important to think about what you’d like to happen to your wealth when you die. For example: — What should any surviving spouse or partner inherit? — Who are your (other) chosen beneficiaries? — Are there any specific items you would like to bequeath to particular people? — What framework – if any – is needed for your bequests? For example, you might be happy to leave capital outright to your 40-year-old daughter with a stable job as an architect, but the same may not be true of your 19-year-old son who is still at university. By answering these questions, you’ll greatly help us to structure your estate planning. Your responses may also prompt you to consider whether making lifetime gifts could be a sensible option.

Rely On Us For Inheritance Advice

Like to talk Inheritance?

I am Vincent and would be happy to have a chat about your inheritance funds and suggest ways we might help.

Click Here to Arrange

Client reviews are submitted to, and verified by, Vouched For.